When you have debt, it seems like it is all you think about.

I’m here to teach you my three favourite methods, and also the ones that I prefer and have used with my debts in our family.

Then of course it is up to you to put it into action and take control of your money.

These methods that I describe I’ve actually used with my own debt of £22k credit card debt, which you can read all about here.

Debt consolidation on my own terms was the method I used – we pay off all debts in one lump sum loan arranged ourselves and then paid off the loan completely. This certainly won’t be an option for everyone, and depends on whether this option is available to you and how much debt you are currently in – but for us it worked and worked quickly.

We ended up paying off that loan within 3 years rather than the projected 5 years, and a great motivational tool to throw money at the loan to clear it.

Debt consolidation loans arranged by third parties may seem like a good idea, but sometimes there is a fair amount of hidden fees that you are paying for the privilege of – so that is why I recommend the below debt repayment options so you are not taken advantage of.

// Debt Management – Never make just the minimum payments if you can

The tricky part of debt is that when you sign up for it you don’t really imagine what you are signing up for.

When the bank manager tells you it is 25 years on a mortgage, you only really listen to the “monthly amount” and then switch off.

But as we all know, the bank and credit card companies make their money from you by hoping you will have that debt for as long as possible, so they can keep charging interest payments to the amount outstanding.

It is well-known that if you only made the suggested minimum payments on credit cards, it might even take you up to 25-30 years to pay off the original one time debt.

That is insane!

Only get into debt for things that truly matter.

Personally I see that as being your education and your home, then everything else should be cash-flowed (save aside money and then spend it). The pain of not having the item temporarily will be far less than the pain of debt on your shoulders to pay off monthly.

Never use credit cards to make it through the end of the month if you can, as you need a plan if an emergency should happen and you are stuck for those payments head.

Commit to never paying just the minimum payment, as this will be you only usually paying off the interest charge and nothing else.

// Know exactly how big your debt is at all times

This may be the hardest part and most painful but you will need to do it and face facts with any credit card debt.

Start a spreadsheet or write down all the locations you believe you have debt and write down the exact amounts required to close the credit cards or loans down completely.

You may need to phone companies or credit cards and tell them you are working to pay back the debt fully. Do not let them give you further credit of course, it is time to get rid of it only.

Find out at this point from the companies what are the absolute minimum payments you need to make each month and write those down on your notepad or spreadsheet.

I understand the struggle of this stage and making the mindset to get out of debt – and that’s why I created a spreadsheet that will change your financial future.

It is called the AutoPilot Money system, and you can download here on my website or on my Etsy store.

http://bit.ly/goalsspreadsheet

// Know your current state of spending and debt, and create a new plan

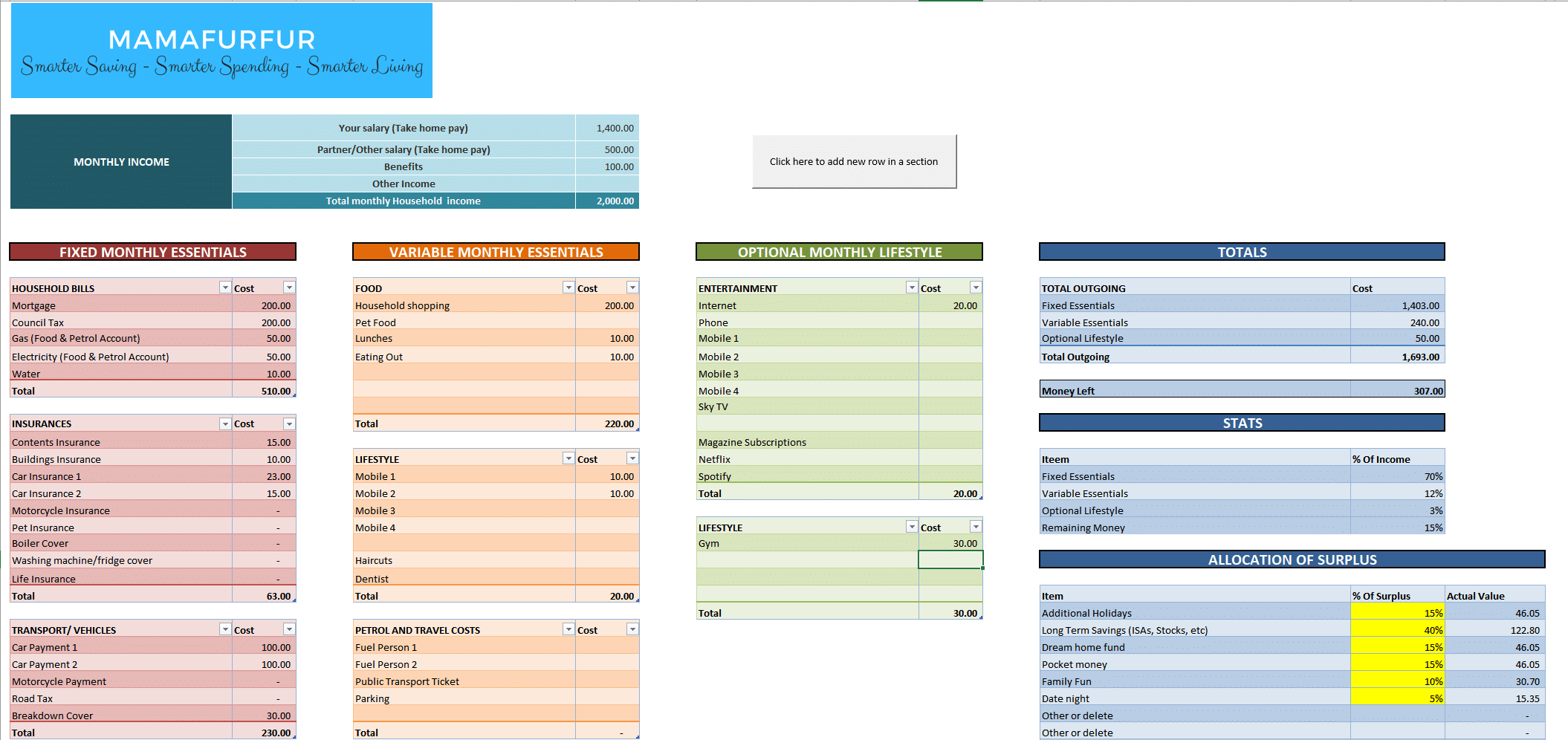

Now we have faced the pain of what we owe, even if that is just a home and/education left, we have to know our current state of spending habits so we can then change it to what we want to achieve and hit our financial goals.

For example, using my AutoPilot Money spreadsheet you can have one location to write down your full budget and see any problem areas at a glance.

Look at your past three months of spending patterns on your current account and credit cards.

If your income is less than your outgoings – you have a problem to solve regardless of how much you earn!

Your outgoings will be your downfall unless you change it today!

For example, the first time you do your current spending you might not like the amounts you see written down.

You might be spending WAY too much on eating out, or on clothes and luxuries.

Next then it is time to squeeze that spending report (budget) to what you want to achieve and see.

BE HONEST WITH YOURSELF – if your goal is to be debt free as quickly as possible YOU NEED TO STRIPE BACK YOUR PLANNED SPENDING MOVING FORWARD AS MUCH AS POSSIBLE. It will be short term pain for long term happiness.

You can see exactly your ideal month and how much you are allocating for each of the areas in your life right now, and below is just an basic example (not the ideal by any means).

You can see on this example we have car payments that really we need to look at removing to free up more of our money for things that matter to us for our goals (financial freedom or investing in our future perhaps).

Below is a snippet of the information you can create like the one below and more detail later on this where you can use this tool to change your financial future. You can use the spreadsheet I created to clearly see how you are using your money right now and also how to tackle any debts, plan for financial freedom and when you will achieve financial freedom based on current habits and planning:

// What to do if you can’t meet minimum payments

If you are looking at your debt right now, and you have no way to squeeze enough of your budget to pay the minimum amounts only – then really my first place of advice is you need to look for another income source first of all.

You may have no other option but to take on an evening job delivering food, or babysitting and tutoring – anything to get money in for the exclusive purpose.

You need to do all you can to pay back the debts without anyone setting in to help you.

If you believe you have no way to make that happen, and to be honest that would only be in extreme cases, then you would be best to speak to your debtors directly.

Phone them and explain you want to pay back the debt fully but struggling to make the minimum payments.

Usually they will agree to a payment system you can commit to, say £5 a week or similar, and then you are under a commitment to make that. If you do not, and the company has given you some flexibility they are within their rights to seek the money directly from you via court judgement and such.

We do not want that to happen, as that can stay on your credit score for many years.

If you are not able to secure a voluntary agreement with the companies, then I would suggest speaking to Citizen’s Advice for honest straight forward options for you or Christians Against Poverty for impartial advice.

Do not take advice from Debt management companies without seeking impartial advice as usually they will try to have you agree to IVAs or similar that will have hidden fees/charges that benefit them.

// Create a small emergency buffer as first stage (Prevent new debt)

Habits of overspending from our income have created the debt we are in now, so the first priority needs to be getting some cash behind us to prevent further use of credit cards or loans.

I suggest that a critical step is to save a minimum of £500-£1000 in a quick access cash account in case the car breaks down, the washing machine fails etc.

It is emergencies only though!

// Squeeze that budget to every last penny!

When you are honest with yourself, you probably know that the debt was created to make yourself feel better or happier.

Whilst we deal with the debt in a very practical way, also use the time without certain luxuries to think about what truly makes you happy instead of spending on things that don’t ultimately bring you joy.

Once we have squeezed every last penny free from our budget, have our emergency fund stored, it is time to attack the debt full speed.

In my AutoPilot Money spreadsheet I created a section exclusively for this purpose, to tell you how to pay off your debt as efficiently as possible.

This part of the spreadsheet shows you how much to pay off each card/loan month at a time, provides you with the debt free date and how much money in interest you will save as a result.

You need to input your debts, interest rates, minimum payments and then decide how much total you are paying to debts each month.

You can then use the Avalanche or Snowball method to clear them off – more about these two methods below.

// Create more money to throw at the debt – you are completely responsible for your past actions

Your spending income is not your final amount here – the game is not over.

Previously we had borrowed from others to run up the debt we have now – time to change those habits and take full responsibility for the money into our lives.

I want you to brain storm 25 ways to make money come into your life and you will need to sacrifice something. As they say nothing comes for free!

This could be selling items on Ebay that you don’t need; offering tutoring or babysitting services to friends; walking more and using transport costs normally occurred to throw at your debt; starting an Etsy store or selling digital products; offer skills on Fivrr for Admin or website work – really use your creative powers here and look at your hobbies and gifts that could help others and would be willing to pay for your time.

Pick 1-3 ways you have brainstormed and commit for the next 30 days to try them out completely and aim to make some money for them.

Look for more ways for money in your life and be open to opportunities that only require your skill set and not money to start up!

// Pick a Debt Repayment Model and commit

We have brainstormed more ways to bring even more money exclusively for the goal of paying back debt into your life, now it is time to set that plan of payments into action.

You can pick from one of three methods based on your level of debt and final goals – the Avalanche, Snowball or Snowflake method.

// The Avalanche Method – Highest interest rate first

The Avalanche Method is used to describe when you want to tackle the debt with the largest interest percentage attached to it first with any extra amounts, once you have made minimum payments on everything outside of that.

For example if you have a mortgage at 2% interest, and a credit card debt at 19% – you would attack the credit card debt first with any spare cash.

Reason being that the credit card over time will keep growing with interest (additional charges) faster than the other debt.

You want to get rid of the option of those debts growing, as this is one way to do that.

// The Snowball Method – Smallest debt first

This method if you imagine is like how you create a great snowball perfect for a play fight.

You start with a small amount then add to it and add to it, until it becomes larger and larger.

With the snowball method, you would look at all your debts, make the minimum payments to them all, and attack the smallest debt first with any extra payments until it was gone.

Once you have that debt paid off, you would move onto the next smallest and so on.

You would never reduce though the total amount of money you spend on debt repayment, unless you absolutely had no choice, as that money starts to take out more and more debts.

This method works for people as you get a sense of pride and joy when you see one debt completely gone, but it doesn’t take into account interest side of debts and for that reason doesn’t work for everyone.

// The Snowflake Method – tiny pieces over a long time

This is another highly successful method where each day or frequently you send small amounts to your debt that you might not have noticed in your spending.

For example, rather than spending £3 on a morning coffee you bring your own into the office at the start of the day, and send the £3 to the debt that day instead.

Those small amounts add up over time and could mean an extra £100 quickly being sent to debt with a few spending habit changes.

You can also have Zero spend days, where you aim to not spend anything and then send the “saved” money over to the debt.

// Low interest credit cards are another option

You may have the option available to you to move all the debt onto one 0% or low interest credit card also. You usually will pay a balance transfer fee (a fee added by the company by moving the money across to the new card) so always make sure you do your sums and figure out if that would help.

Usually with 0% interest cards, you receive that benefit for a limited time only – so if the length of time and debt can be paid fully then this might be a good option for you.

For example, if you believed you could pay off all the debts comfortably and could receive a 0% card with the balance transfer fee being smaller than the relative interest of the current debts, that route would allow you to see the debt in one place and be a great motivator. You would then use normal one large monthly payment to clear it and factor as much money as you can at the debt (don’t pay the minimum only!).

// Home and education – My 10% Debt repayment Method as standard – Add that little extra for full effect

My personal method now that we only have our mortgage and car payments to make, our credit card debt is gone thankfully, is to use my 10% extra method.

I commit to making the minimum payments on everything and then 10% monthly payment on top regardless of the interest level or size.

That 10% extra adds up and without noticing you end up making an extra ONE Payment a year and then some.

When I have extra money to use towards debt repayments, I also consider the money return potential.

If I would gain a better return on money by placing it into an Investment account (normally 5-10%) compared to the interest on my debt (perhaps 2% for a mortgage) – I will invest it instead to later use the money to repay my mortgage in the future.

**This is just my preferred reasoning though, and not absolute advice for all circumstances.**

// Decide on better money spending habits – the 80/20 spending report

I believe strongly that any budget and household can use their money to create incomes in the future and to pay off debt right now.

Our household works to a 80/20 principle ideally where we use 80% of our monthly incomes to pay off debts, live happily, have experiences and then the other 20% is used for our future in investing or likewise.

If you are in a lot of debt right now, I strongly advise throwing as much money as you can to your debt though as we want that to be gone for good, to help our security right now and also to not hold the weight of our past habits with us any further.

If you just have a mortgage as your only debt, I would then suggest building your future through investments and higher interest savings accounts.

By changing your goal from debt repayment to financial future building – being able to use your savings to auto generate an endless amount of cash that you need to live – you then create a brighter future for your family and life.

You can follow Our Journey to Financial Freedom and security on this blog monthly of course, to learn some tips and tricks for your family too.

New to Investing or how to start working on your future – let me show you how here.

{kind=link}